This is my take on Rogoff’s “Modern Monetary Nonsense”

Rogoff: “A number of leading US progressives, who may well be in power after the 2020 elections, advocate using the Fed’s balance sheet as a cash cow to fund expansive new social programs, especially in view of current low inflation and interest rates.”

Rogoff’s use of the expression “as a cash cow to fund” ignores the fact that the Fed is already the “cash cow” that makes all economy’s payments possible. The Fed lends to banks when they purchase banknotes, when they buy Federal Treasuries, or when they pay taxes on behalf of their clients. All “base money” needed to make payments comes from the Federal “cash cow” Reserve.

2

Rogoff then quotes, in agreement, Powell: “The idea that deficits don’t matter for countries that can borrow in their own currency I think is just wrong”.

Yet again, where is the exception? All countries whose institutions are politically stable are capable to borrow from residents in their own currency (This, by the way, is made possible by a loan of the central bank to the banks). Residents may then sell their Treasuries to foreigners, and the foreign sector may be willing to accumulate a stock of Treasuries if they desire to hold that particular currency. The consequence will be a higher value of that currency than otherwise, not any kind of enhanced ability of the government to borrow.

3

Again, Rogoff: “The US is lucky that it can issue debt in dollars, but the printing press is not a panacea.”

The luck is that they can buy from foreigners much more than what they sell, with no dollar depreciation. The printing press is not part of the picture.

4

Rogoff continues: “If investors become more reluctant to hold a country’s debt, they probably will not be too thrilled about holding its currency, either.”

Yes, but to put it more precisely, and with reference to national (federal) public debt and not to regional administrations’ debt (so this does not apply to the euro area), foreigners’ willingness to hold a country’s debt depends on their willingness to hold its currency. Holding public debt is the safest way to hold any currency.

5

Rogoff again: “If that country tries to dump a lot of it on the market, inflation will result.”

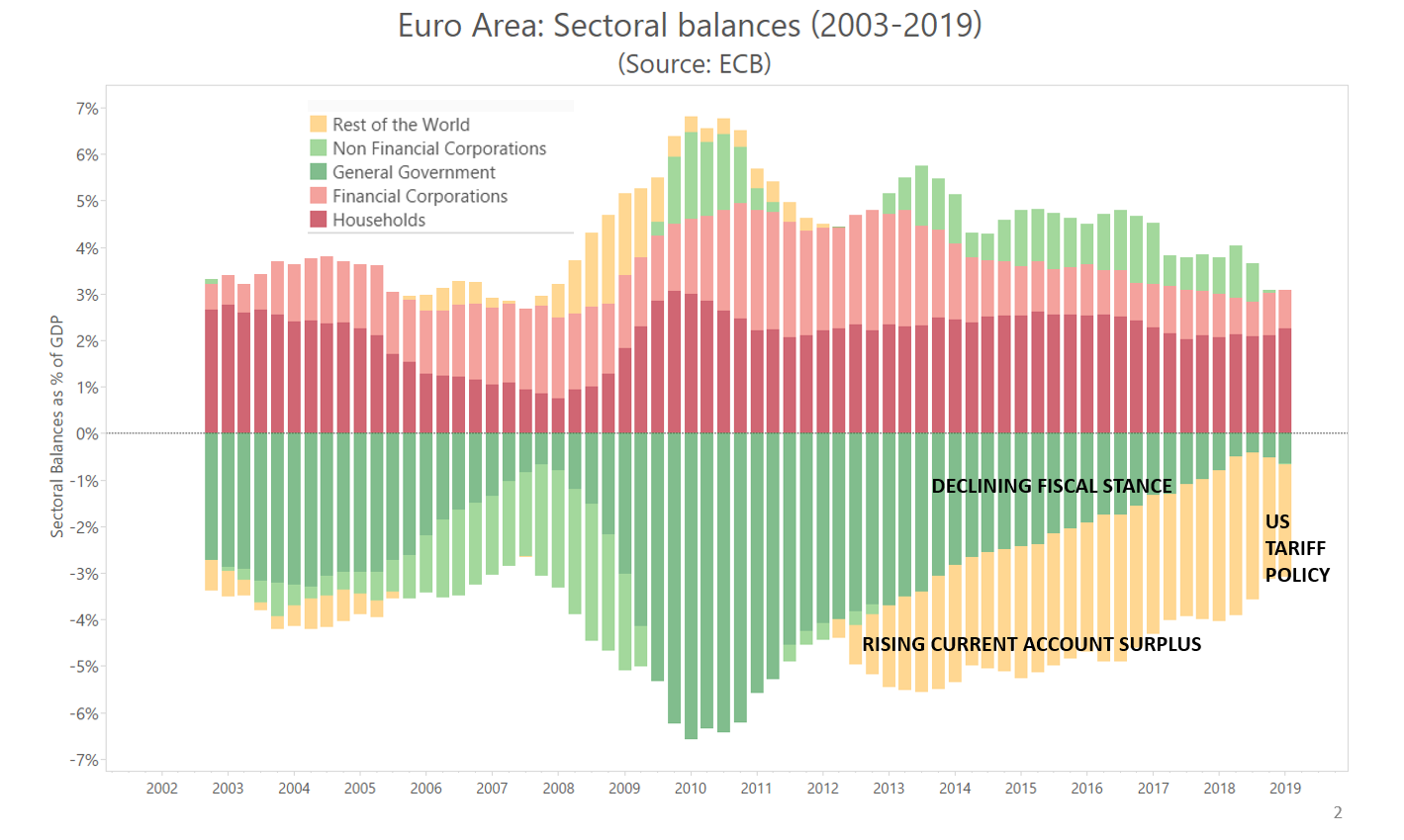

Rogoff leaves this unexplained. Dumping a currency (in the form of public debt or other assets denominated in that currency) will lower the value of that currency in the foreign exchange market. This may raise domestic prices if the country is highly dependent on imports that become more expensive with depreciation. Or may not. When China dumped euros at the time the ECB started its Asset Purchase Program, the foreign value of the euro went down but not much inflation followed.

6

And Rogoff: “While in “Japan […] most debt is held domestically, the US […] depends heavily on foreign buyers.”

The value of the dollar (not the financing of public debt) depends on foreign dollar holders. Foreigners hold dollars in various forms (public debt and private debt) and dollars are claims on the Fed and the U.S. government. When foreigners are tired to hold them, they can use them to purchase US goods, services, or real assets. But foreigners are not making Federal borrowing possible.

7

Finally, a light of truth from Rogoff: “QE, when it consists simply of buying government bonds, is smoke and mirrors. The Fed’s parent company, the US Treasury Department, could have accomplished much the same thing by issuing one-week debt, and the Fed would not have needed to intervene.”